Cantabil Retail India Limited (Cantabil) was established in February 1989 as a private limited company, dealing in wholesale of garments and accessories. Cantabil’s journey is closely linked with the entrepreneurial journey of its founder, Vijay Bansal.

Born in Jind, Haryana, he completed his B.Com in 1979 and initially joined his family’s grocery business. However, instead of continuing in traditional retailing, he started building a distribution business by taking agencies of well-known FMCG brands such as Colgate and Hindustan Lever. Selling products door-to-door gave him deep practical experience in sales, customer behaviour, and distribution, helping him develop the confidence to understand why products succeed or fail in the market.

In 1986, he moved to Delhi and opened a Liberty shoe showroom in Connaught Place. Around the same time, he entered the garment accessories business, becoming a distributor of zippers and polyester buttons. As India’s garment export industry expanded, this business became highly profitable and allowed him to build both industry relationships and capital.

Working closely with garment manufacturers gradually sparked his interest in apparel retail. In 2000, he launched the Cantabil brand.

Cantabil Retail Limited, established in 2000, stands as a prominent figure in India’s apparel retail sector. Recognized for its blend of trendy yet affordable clothing catering to men, women, and children, Cantabil has secured a robust nationwide presence. Offering a diverse array of products spanning formal wear, casual attire, and accessories, Cantabil ensures its appeal to a broad consumer base. Through an extensive network of exclusive brand outlets, franchise stores, and online platforms, the company ensures widespread accessibility to its offerings.

The Cantabil brand offers the complete range of formal-wear, party-wear, casuals & ultracasual clothing for Men and Women in the middle to high income group.

Initially, Cantabil sold through multi-brand outlets (MBOs), but the response was disappointing. The management then changed strategy and started opening exclusive brand outlets (EBOs). This proved to be a turning point, as customers responded much more positively to dedicated Cantabil stores where the company could showcase its full product range and create a consistent brand experience.

To enhance its presence in new geographies and to fund this expansion, CANTABIL came with an IPO in Sept 2010 which had 411 stores on 31 st Mar 2010 and it reported revenue/ EBITDA/ PAT of INR 202 cr/ INR 31 cr/ INR 15 cr in FY10. The average revenue per store stood at INR 55 lacs, while EBITDA and PAT margins were 15.2% and 7.3% respectively and asked a fresh issue size of INR 105 cr, which was planned to be utilized in the following manner:

- INR 32 cr for the establishment of a manufacturing facility at Bahadurgarh, Haryana

- INR 25 cr for the expansion of the retail network by 180 new stores (80 stores in FY11 and 100 stores in FY12) in Hyderabad, Bengaluru, Cochin, Nagpur, Pune, Vishakhapatnam, Patiala, Bhatinda, Chandigarh, Lucknow, Kanpur and Varanasi.

- INR 30 cr for additional working capital

- INR 20 cr for the repayment of debt.

How Cantabil Survived Its Toughest Phase (2011–2014)

Cantabil’s IPO in 2010 was followed almost immediately by one of the worst periods for India’s organised apparel retail industry.

Between 2012 and 2015, consumer demand slowed sharply, several retail chains either shut down or went through severe financial stress, and discretionary spending weakened. Cantabil was caught in this industry-wide downturn and reported cumulative losses of nearly ₹70 crore over the next three years.

However, according to the management, the difficult period was not solely because of weak industry conditions. It also exposed weaknesses within Cantabil’s own business model.

The company had expanded aggressively and was operating nearly 300 Cantabil stores along with around 200 stores under its Lafanso brand. A significant number of these stores were either poorly located or generating inadequate returns, resulting in a large fixed-cost burden. Instead of contributing to profits, many stores became a drag on the business.

At the same time, inventory management had become a major issue. Merchandise had accumulated to such an extent that the company had enough stock to keep selling for almost an entire year without manufacturing fresh products. Large amounts of capital were locked in unsold inventory, reducing operational flexibility and increasing pressure on profitability.

The crisis also forced the company to reassess what customers actually wanted. Management realised that success in apparel retail was not only about opening stores it depended equally on merchandise quality, store presentation, and customer experience.

The Turnaround: Building a Leaner and More Efficient Business

The restructuring undertaken during FY12–FY14 fundamentally changed the trajectory of Cantabil. Instead of chasing growth through rapid store expansion, the management shifted its focus towards building a leaner, more efficient, and profitable business.

To reduce cost pressures and improve store-level productivity, the company embarked on a comprehensive restructuring exercise. It rationalised its retail footprint by reducing the store network from 500 stores in FY10 to just 143 stores by FY14, exiting underperforming locations that diluted profitability. At the same time, employee strength was reduced from 1,100 to 885, aligning the cost structure with the smaller store base. Inventory management also became a key priority, with inventory days declining from 217 days to 153 days, reducing working capital as a percentage of sales by nearly 1,168 basis points to 41.8%.

The management complemented these financial measures with several operational improvements. It shut down nearly 150 Cantabil stores and 200 Lafanso stores, drastically reduced fresh production to only 10–20% of normal levels while clearing accumulated inventory with deep disocunts, became far more selective in product development, the company therefore upgraded store interiors, replaced furniture, improved visual merchandising, enhanced product quality, and focused on creating a better shopping experience. According to the promoter, the impact was visible almost immediately, with newly introduced products selling as soon as they reached stores.

This difficult period proved to be a defining moment for the company. Having learned the cost of indiscriminate expansion, the management adopted a disciplined and highly selective approach towards opening new stores. Every expansion decision was now evaluated based on long-term profitability rather than short-term growth.

The Turnaround Begins to Show

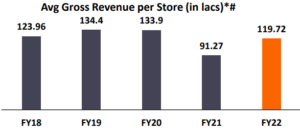

The results became evident over the next five years. Between FY14 and FY19, Cantabil’s revenue grew at a 21% CAGR to ₹289 crore, while the store network expanded in a measured manner from 143 stores to 241 stores. More importantly, average annual revenue per store increased significantly from ₹75 lakh to ₹1.3 crore, highlighting a substantial improvement in store productivity rather than growth driven purely by adding more outlets.

Profitability also improved sharply during this period. EBITDA turned around from a loss of ₹3 crore to a profit of ₹30 crore, while PAT improved from a loss of ₹9 crore to a profit of ₹13 crore. Consequently, EBITDA margin expanded to 10.3%, while PAT margin reached 4.3%, reflecting the benefits of improved operating leverage and tighter cost controls.

The balance sheet also became considerably stronger. Despite investing approximately ₹65 crore in store expansion between FY14 and FY19, the company maintained a conservative financial profile. The working capital cycle reduced from 152 days to 84 days, while working capital as a percentage of sales declined from 41.8% to 22.9%. Net debt-to-equity improved from 0.43x to 0.34x, and capital efficiency strengthened meaningfully, with ROE improving from -4.4% to 10.3% and ROIC increasing from 4.5% to 13.5%.

Cantabil’s turnaround demonstrates that sustainable retail businesses are built not by opening the maximum number of stores, but by maintaining disciplined expansion, efficient inventory management, prudent capital allocation, and strong unit economics. The restructuring between FY12 and FY14 laid the foundation for the company’s long-term, profitable growth.

As on 31 March 2020, Cantabil operated 221 COCO EBOs (covering an area of 2.49 lakh sqft) and while another 81 (with an area of approximately 76,000 sqft) were under the FOFO model across 16 states with the strongest growth coming from operations in Tier 2 and 3 cities.

Cantabil has a manufacturing plant with an area of 1.5 lakh sqft in Bahadurgarh, Haryana, with an annual production capacity of 10 lac pieces of garments per annum

- Casual trousers capacity of 3 lac pcs per annum

- Formal trousers capacity of 2 lac pcs per annum

- Suits & jackets of 2 lac pcs per annum

- Shirts capacity of 3 lac pcs per annum

CANTABIL has two centralized warehouses in Haryana and Delhi to ensure seamless and timely logistics and two centralised warehouses to ensure seamless and timely logistics. The production facility has fully-integrated infrastructure and systems with complete automation required for modern manufacturing and retailing operations. The Bahadurgarh plant is currently running at full capacity. Besides its own manufacturing capacity, the company outsources jobwork to two large dedicated fabricators and some smaller units. Canabil’s annual overall manufacturing capacity is 1 million garments.

In FY20, 84% of Cantabil’s revenues came from men’s wear, 11% from women’s wear, 3% from accessories and 2% from kidswear. The region-wise sales split was: North 65%, West 28%, East 3%, Central 3% and South 1%

By employing efficient supply chain and cost-effective sourcing strategies, Cantabil maintains competitive pricing without compromising on quality. Its commitment to innovation allows it to adapt swiftly to changing fashion trends and consumer preferences, ensuring continued relevance in the market. Despite market fluctuations, Cantabil has demonstrated consistent profitability, showcasing resilience and adept financial management.

With its strong market presence, growth potential, and commitment to ethical business practices, Cantabil Retail Limited remains a significant player in India’s apparel retail landscape.

A distinctly visible strategy of CANTABIL to tap under discovered markets of Tier II & III cities of India (often neglected by foreign & marquee brands) is gaining momentum. The company has a network of 414 exclusive retail outlets (as on 31st Aug 2022) covering an area of 4.6 lac sq ft in 18 states (up from 241 stores & 2.6 lac sq ft area in FY19.

FY19-22: Maintained consistency in revenue performance During FY19-22, CANTABIL’s revenue grew at a CAGR of 9.9% to INR 383 cr driven by aggressive store expansion across India from 241 stores in FY19 to 378 in FY22. However, COVID-led restrictions impacted average revenue per store, which declined to INR 1.19 cr in FY22 (CAGR decline of 6.8%) from INR 1.34 cr recorded during FY19.

CANTABIL’s strategy of operating through a mix of owned and franchise stores enables it to effectively manage capex and opex, diversify risk and expand faster. The company maintains a 80:20 mix between COCO and FOFO and we see this as a credible strategy which enables it to balance its capex and opex burden while being able to expand its store network across India at a faster pace.

Execution Becomes the Competitive Advantage

The turnaround years had fundamentally changed Cantabil. By FY23, the company was no longer fighting to repair its balance sheet or prove that its business model worked. Those questions had largely been answered. Instead, management faced a different challenge could the company continue growing at a healthy pace while maintaining profitability in an industry that had once nearly brought it to its knees?

Ironically, the environment was once again becoming difficult.

The post-pandemic demand boom that had benefited most apparel retailers had begun to fade. Inflation continued to weigh on discretionary spending, particularly in the mass and mid-premium segments. Consumers became increasingly cautious, festive demand remained inconsistent across several regions, and unseasonal weather disrupted one of the most important sales drivers for apparel companies the winter season. Across the industry, retailers responded with aggressive promotions and discounting to stimulate demand, putting pressure on margins and profitability. Management repeatedly acknowledged that the retail environment remained subdued despite India’s strong long-term consumption story.

For Cantabil, however, this period looked remarkably different from the slowdown it had experienced a decade earlier. During FY12–FY14, weak demand had exposed structural weaknesses in the business. By FY23, the company had already spent several years rebuilding those foundations. Instead of reacting to short-term market conditions, management chose to execute the long-term playbook it had been refining since the turnaround.

Rather than slowing expansion, Cantabil continued strengthening its retail network. During FY24, the company opened 86 new Exclusive Brand Outlets (EBOs), taking its presence deeper into Tier II and Tier III cities, where organised apparel penetration remained relatively low. Unlike the aggressive expansion of the pre-2012 era, each new store was evaluated with significantly greater discipline, focusing on location quality, catchment potential and long-term profitability rather than merely increasing the store count.

Management also recognised that future growth could not depend solely on adding more stores. The company therefore focused on expanding the overall shopping basket. Traditionally known as a men’s apparel brand, Cantabil steadily increased its presence in women’s wear, kids’ wear, footwear and accessories, gradually transforming itself into a complete family fashion destination. Larger store formats allowed the company to display a broader assortment, encouraging higher basket values while improving customer convenience. This strategy also improved rental efficiency, as larger stores generated better revenue per square foot without proportionately increasing occupancy costs.

Another area receiving increasing management attention was e-commerce. While physical stores remained the backbone of the business, online channels were no longer viewed as a competing format but as an extension of the brand. During FY24, online revenue more than doubled, reflecting improving brand acceptance across digital marketplaces and creating an additional growth lever without requiring significant incremental capital investment.

Perhaps the most striking aspect of this phase was management’s willingness to continue investing despite a difficult operating environment. In FY24, Cantabil strengthened its balance sheet by raising approximately ₹50 crore through a Qualified Institutional Placement (QIP). Rather than using these funds to repair the balance sheet, management positioned the capital as growth capital intended to accelerate store expansion and capture opportunities as consumer demand eventually recovered.

This confidence stemmed from an important observation. While overall footfalls remained subdued, existing customers were spending more per visit. Management highlighted that average bill values had improved despite muted consumer sentiment, indicating that Cantabil’s core customer base remained loyal even during weaker demand conditions. This was an encouraging sign because it suggested that the brand was gradually moving beyond being a transactional apparel retailer towards becoming a preferred shopping destination for repeat customers.

By the end of FY24, the financial results reflected this resilience. Despite operating in one of the toughest demand environments for organised apparel retail, the company delivered 12% revenue growth, continued expanding its store network, strengthened its capital base and improved its online business without compromising financial discipline. The performance may not have appeared extraordinary in isolation, but it demonstrated something arguably more important the operating model developed after the turnaround was capable of delivering consistent growth even when the broader retail environment remained challenging.

Accordingly, management unveiled Vision 2027, outlining an ambition to cross ₹1,000 crore in annual revenue by FY27. Unlike the aggressive expansion plans that had characterised the company’s earlier years, this roadmap was built around clearly identifiable operating levers rather than optimistic assumptions. Revenue growth was expected to come from four key pillars: healthy Same Store Sales Growth (SSSG), continued expansion of the store network, increasing contribution from e-commerce, and deeper penetration of women’s and kids’ apparel. The strategy reflected a notable shift in thinking. Instead of simply opening more stores, management focused on extracting higher productivity from every square foot of retail space.

One of the most important changes during this period was the evolution of Cantabil’s store format. Over the years, the company had realised that larger family stores consistently outperformed smaller outlets. Bigger stores enabled the company to showcase a wider assortment across men’s, women’s and kids’ categories while improving customer convenience through one-stop family shopping.

More importantly, larger stores generated superior economics. Rental costs did not increase proportionately with store size, allowing occupancy costs as a percentage of sales to decline while improving operating leverage. Rather than maximising the number of stores, management increasingly focused on maximising the productivity of each store by increasing the store size from 1300 sq ft to 1600 sq ft. This was a stark contrast to the expansion strategy that had contributed to the company’s difficulties a decade earlier.

Execution during FY25 increasingly validated this strategy.

Although the broader apparel industry continued to experience uneven consumer demand, Cantabil consistently outperformed through improving store productivity rather than relying solely on network expansion. Same Store Sales Growth, one of the most closely tracked indicators in organised retail, steadily strengthened through the year. After beginning the year with healthy growth, the company reported an exceptional 17.7% SSSG during the third quarter of FY25, indicating that existing stores not just newly opened outlets were contributing meaningfully to revenue growth. This was particularly encouraging because SSSG is often regarded as one of the clearest indicators of brand acceptance and customer loyalty. Strong SSSG meant customers were returning to existing stores more frequently and spending more, rather than growth being driven purely by opening additional locations.

Management attributed this improvement to several operational initiatives undertaken over the preceding years. Product assortment had become significantly sharper, inventory planning had improved, and the company was introducing collections more closely aligned with customer preferences. The expansion of women’s wear and kids’ apparel also encouraged family purchases, increasing basket sizes without requiring additional customer acquisition. Simultaneously, the company continued enhancing the in-store shopping experience through better layouts, visual merchandising and larger format stores, reinforcing customer engagement.

Another important development was the increasing contribution from repeat customers. During interactions with investors, management indicated that nearly half of Cantabil’s business now came from repeat customers. For an apparel retailer operating in a highly competitive market, this represented a significant competitive advantage. Repeat customers reduce marketing costs, improve demand visibility and generally indicate that product quality, pricing and customer experience are resonating with the target audience. Rather than chasing growth through heavy discounting, Cantabil appeared to be building a loyal customer base capable of supporting sustainable long-term expansion.

Perhaps the most notable financial development during FY25 was the steady expansion in profitability. While many retailers resorted to promotional discounting to stimulate demand, Cantabil managed to improve margins through operational efficiencies instead of price-led growth. EBITDA margins gradually expanded from around 26% in FY24 to over 28% by FY25, reflecting the combined benefits of operating leverage, disciplined sourcing, better inventory management and improving store productivity. The improvement was not driven by a single extraordinary event but by multiple incremental efficiencies accumulated over several years.

Inventory management, a weakness during the company’s troubled years, had now become one of its operational strengths. Better demand forecasting reduced excess inventory, allowing the company to minimise end-of-season discounting while maintaining healthier gross margins. Simultaneously, higher sales throughput improved inventory rotation, reducing the amount of capital locked in working capital. As volumes increased, Cantabil also benefited from stronger procurement efficiencies and manufacturing leverage, further supporting margin expansion

By the end of FY25, the narrative surrounding Cantabil had changed meaningfully. The discussion was no longer centred on whether the turnaround was sustainable. Instead, attention gradually shifted towards the scalability of the operating model. With improving SSSG, expanding margins, healthier store economics and a clearly articulated roadmap, the company entered FY26 with growing confidence that the business model it had patiently rebuilt over the previous decade was now capable of supporting its next phase of growth.

Execution Becomes the Competitive Advantage

The significance of FY26 was not that the company reported another year of growth. Rather, it was that the growth came despite an operating environment that remained far from ideal. Geopolitical uncertainties disrupted global supply chains, input costs remained volatile and discretionary consumption continued to witness periodic weakness. Yet, instead of slowing down, Cantabil delivered its strongest financial performance in the company’s history.

Revenue crossed ₹850 crore, growing nearly 18% year-on-year, while EBITDA increased by almost 29%, taking EBITDA margins to 31%. PAT also reached a record level, growing by approximately 28%, with PAT margins improving to 11.2%. More importantly, these were not isolated quarterly numbers. Management highlighted that since FY22, revenue had compounded at roughly 22% CAGR, while PAT had grown at nearly 26% CAGR, indicating that profitability was expanding faster than revenue. This was perhaps the clearest evidence that the operating model had matured.

The obvious question, however, was what changed?

Unlike many apparel retailers where margins fluctuate primarily because of pricing or discounting, Cantabil’s margin expansion was largely operational.

The first driver was store economics. Over the previous few years, management had consciously increased the average store size. Larger family stores enabled the company to merchandise a broader assortment across men’s, women’s, kids’ wear and accessories while simultaneously improving occupancy efficiency. Since rentals do not increase proportionately with area, larger stores generated better revenue per square foot and superior EBITDA contribution. Instead of opening the maximum number of stores, management focused on opening the right stores.

The second driver was product mix. Historically, Cantabil had been predominantly a men’s apparel brand. By FY26, they starter focusing on women’s wear, kids’ wear, footwear and accessories. These categories not only diversified revenue but also increased average basket size, as entire families could complete their purchases under one roof. This strengthened the company’s positioning as a family fashion retailer rather than a men’s apparel chain.

Another notable aspect of FY26 was that growth was not driven purely by opening new stores. Existing stores continued to perform well, with healthy Same Store Sales Growth supported by higher average bill values and a loyal customer base. During investor interactions, management indicated that nearly 50% of sales now came from repeat customers, a metric that reflected the growing strength of the brand. In apparel retail, where customer acquisition costs continue to rise, a large repeat customer base provides both revenue visibility and resilience during weaker demand cycles.

Operational improvements were equally visible in the company’s capital efficiency. Despite maintaining an aggressive expansion strategy, Cantabil remained virtually debt free while improving its return ratios. This represented a remarkable transformation from the years immediately following the IPO, when excessive expansion had strained both profitability and the balance sheet.

Perhaps the biggest takeaway from FY26 was not the absolute financial performance but the increasing credibility of management execution.

Throughout FY23 and FY24, management repeatedly spoke about Vision 2027, outlining a roadmap to achieve ₹1,000 crore in revenue through a combination of healthy Same Store Sales Growth OF 5%, disciplined store expansion, larger store formats, deeper penetration into women’s and kids’ categories and continued growth in e-commerce. As FY26 concluded, many of these operating drivers were already visible within the business. Management has also spoken about a longer-term aspiration of reaching ₹2,000 crore in revenue by 2030 and doubling its store count from here on, supported by a significantly larger retail footprint and continued improvements in store productivity. Whether those ambitions are ultimately realised will depend on consumer demand, competitive intensity and, above all, execution. The Indian apparel industry remains intensely competitive, with organised retailers, value-fashion chains and digital-first brands all competing for the same consumer. Sustaining growth in such an environment will require the same discipline that helped Cantabil rebuild itself over the previous decade.

Key Risk to Monitor

1.Elevated Inventory Compared With Peers

Cantabil carries relatively higher inventory because it follows a hybrid ownership model where inventory of 20% of franchise stores is also reflected on its books. Since inventory remains owned by the company until sold to end consumers, inventory days naturally appear higher than peers and should be in the ranges of 100-120 days ,who transfer inventory directly to franchisees. Investors should therefore monitor inventory quality and working capital trends rather than headline inventory days in isolation.

2. Execution Risk on Store Expansion

The long-term thesis assumes the company can continue adding approximately 70-80 net stores annually while maintaining 5–7% SSSG. Any slowdown in store additions or weaker mature store productivity could reduce revenue compounding and delay earnings expansion.

3. Free Cash Flow Must Continue Funding Expansion

The long-term expansion strategy remains attractive only if the company is able to generate sufficient free cash flow .Free cash flow generation has remained relatively subdued over the last three years, therefore investors should keep a close watch on cash generation going forward. If the company is unable to fund expansion through internal accruals, it may have to raise capital through debt, equity dilution, or instruments such as preference shares, as was done in February 2024.

CONCLUSION

In many ways, Cantabil’s journey can be divided into three distinct phases.

- The first phase was about building a brand.

- The second phase was about surviving a crisis and rebuilding the business.

- The third phase, which is still unfolding, is about scaling a disciplined operating model.

That distinction is important because today’s Cantabil is fundamentally different from the company that entered the difficult years after its IPO. The lessons learnt during the FY12–FY14 downturn continue to influence management decisions even today. Store expansion has become more measured, inventory management more disciplined, capital allocation more prudent and profitability a far greater priority than simply increasing revenue.

Ultimately, Cantabil’s story is not one of uninterrupted success. It is a story of adaptation. The company expanded aggressively, experienced the consequences of that strategy, restructured itself through difficult decisions and gradually rebuilt a stronger business. The years between FY23 and FY26 demonstrated that this transformation was not temporary. They showed an organisation capable of translating strategy into consistent execution while preserving financial discipline.

Whether the next chapter unfolds exactly as management envisions remains to be seen. But if the company’s journey over the past two decades offers one enduring lesson, it is that sustainable businesses are rarely built by avoiding adversity. More often, they are shaped by how effectively they learn from it. Cantabil’s evolution from an ambitious regional retailer into a disciplined national fashion brand is perhaps the strongest evidence of that principle.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.